Give the Citi Thank You Premier a second thought before applying for the Chase Sapphire (Premier or Reserve)

I have been a very big fan of my Citi Thank You Premier card for the past 2.5 years as more and more of my friends and acquaintances have flocked to the Chase Sapphire family – whether it’s for the Preferred or the Reserve. The Citi Thank You Premier card is often forgotten amidst all the hype of Chase Sapphire referrals, and I wanted to point out a few things worth considering. (While I acknowledge that there are some extreme credit card enthusiasts for whom the Chase Sapphire family of cards vastly outweighs the Citi Thank You cards in benefits, I really believe that the Chase Sapphire is not the right choice for the average 20-something year old.)

First off, if you’re not too familiar with the Chase Sapphire Preferred, I recommend doing a quick search online of the card and reading up (there are some very descriptive blog posts). I’m not going to delve into the details here, and instead will draw a few quick comparisons between the Chase Sapphire Preferred (CSP) and the Citi Thank You Premier (henceforth referred to as the “Citi”).

5 second summary of why Citi Thank You Premier beats Chase Sapphire Preferred

Better points per dollar spent in key millennial spend categories (transportation, travel, entertainment, and gas), comparable points for dining out. Same annual fee, other benefits, etc.

But what about the welcome bonus? Answer here.

How about the Chase Sapphire Reserve? Answer here.

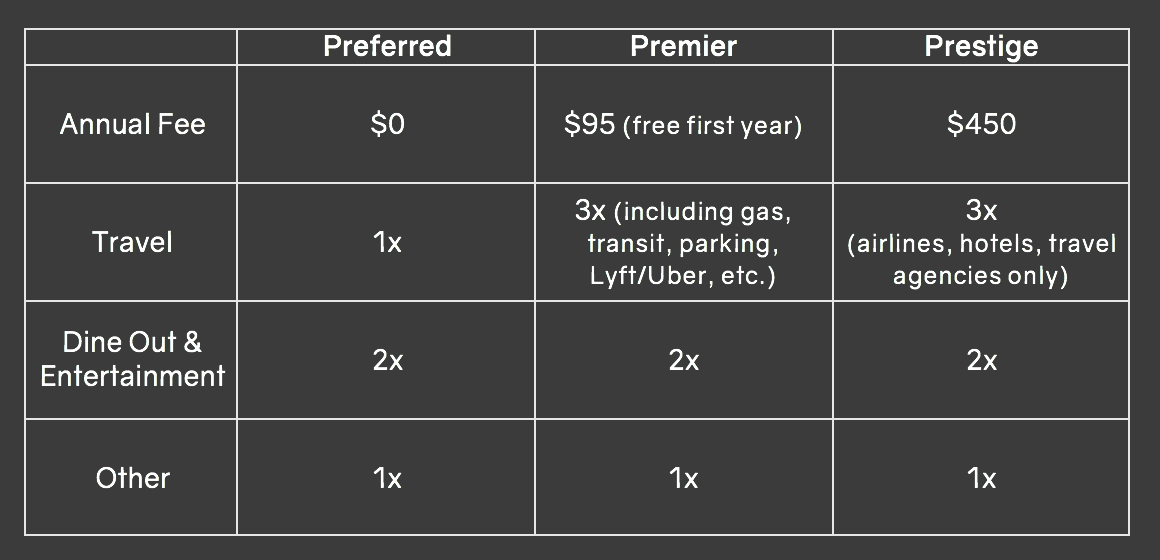

A bit about the Citi Thank You cards

As background, the Citi Thank You family of credit cards has three tiers:

- Citi Thank You Preferred: the baby/toddler card

- Citi Thank You Premier: the rookie card

- Citi Thank You Prestige: the pro card

The really high level comparison here is that the Preferred is a great card to start with if you’re in college or don’t have extensive credit history. The Prestige is likely not a prime candidate if you’re not a huge traveler and looking to benefit from some of its other features, such as its $250 air travel credit, lounge access via Priority Pass Select, Global Entry credit, and 4th night free at hotel stays when booked through Citi (much more similar to the Chase Sapphire Reserve).

All in all, my focus here will be on the Citi Thank You Premier, which is the most apt comparison with the Chase Sapphire Preferred.

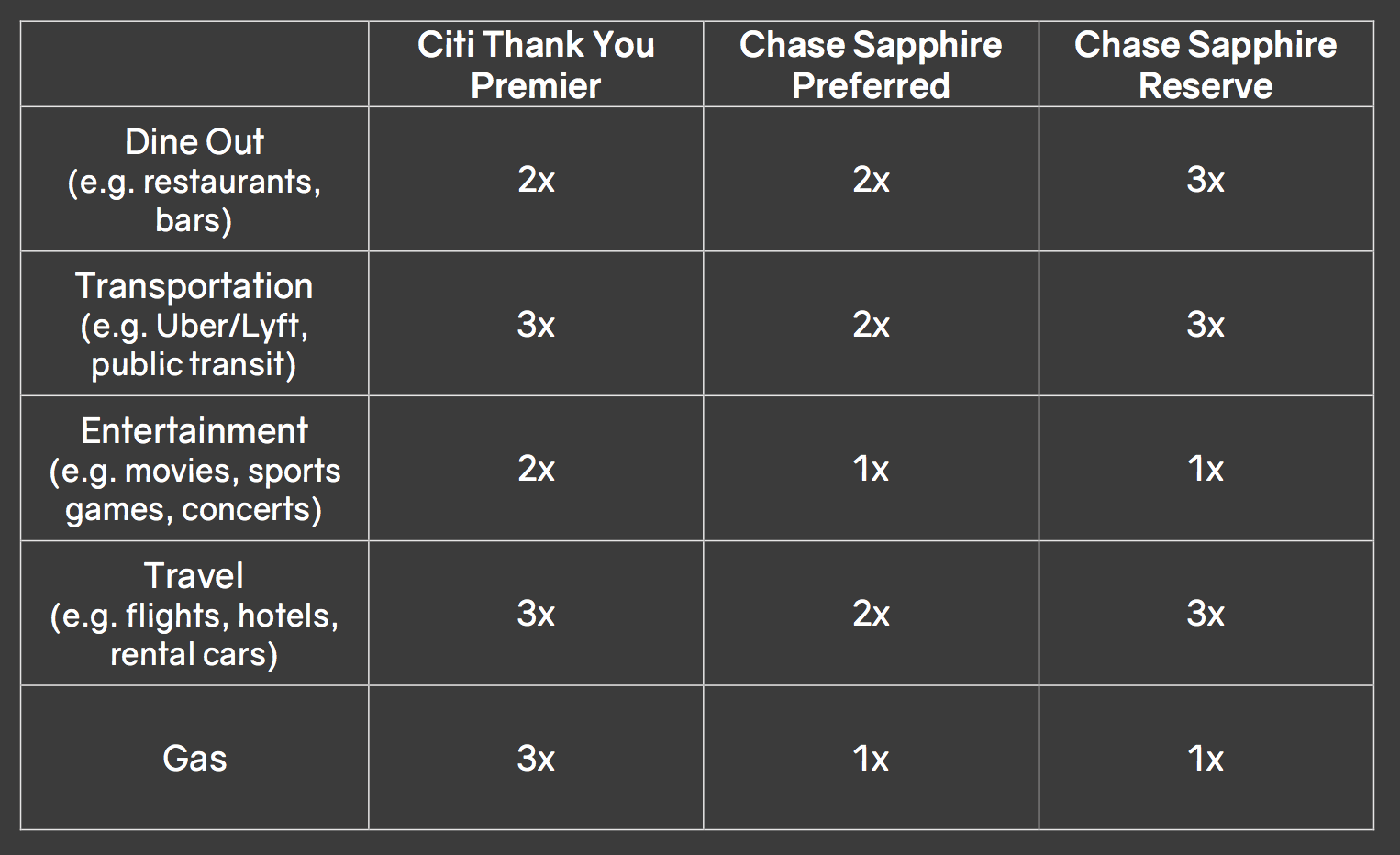

At a high level, the cards may look pretty similar

Both have annual fees of $95, waived for the first year. Both cards reward you with points and the points categories are somewhat similar at a first glance. The most obvious difference between the two cards is probably appearance: one is metal and shinier (CSP), while the other is a “lame” plastic card (though arguably it has the added benefit of not setting off metal detectors). The differences don’t just end there though…

Think about your spend categories

My hypothesis is that the largest spend categories for the average 20-something year old are dining out and transportation, along with occasional entertainment and travel. For the purposes of comparison, I’ll actually lay out both Chase Sapphire cards alongside the Citi.

Keep in mind that the Chase Sapphire Reserve (CSR) is a card that is intended to compete with the Citi Thank You Prestige. See below for my note on the CSR.

The Citi outperforms the CSP on all categories except Dine Out. All else held equal, if you’re paying the same annual fee, wouldn’t you rather get more rewards per category of spend?

Try out this spend/best credit card calculator here, and see how different your rewards would be with the two cards. If you spend $250 per month on dining out, $150 per month on transportation, $500 per year on entertainment, $1200 in travel, and $2000 otherwise…you’ll earn 18k points with Citi versus 14.5k with Chase. With Citi, you’ve also earned 2x your annual fee whereas with Chase you’re only at 1.5x your annual fee.

Regarding the Chase Sapphire Reserve

I find that for most people, the Chase Sapphire Reserve is an unnecessary choice (again, unless you’re an avid traveler and card enthusiast). Frankly, most of the perks it provides (like the Citi Thank You Prestige) are induced demand – would you really need to go to a lounge if you didn’t have free access? Are you really going to complete the Global Entry application process (this requires going for an interview at your nearest major airport…)? (Likely if you wanted it enough you already have it, so it shouldn’t even factor into the credit card calculus. If you don’t currently have it, I’m guessing you won’t be motivated enough to go through this process.)

Think about your habits and how you’ll use your rewards

One of the most common pitfalls I see is people who get drawn into the Chase Sapphire craze, get the card, meet the minimum spend, and then forget to use their bonus points. If you rarely travel, these cards may not be the right option for you because the best redemption value comes from travel redemptions (I’d consider the Citi Double Cash instead). Furthermore, usually credit card points are best used towards airfare – hotels tend not to be priced as competitively when purchasing in points instead of in dollars.

There are two ways to redeem travel through both cards: either through the credit card company’s travel system where you book flights directly or by transferring your points to an airline and then booking travel through the airline. Many card enthusiasts make the argument that Chase points are worth more than Citi Thank You points because of their airline transfer offers. However, I challenge you to stop and think about whether you even know which airlines fly the routes you want to travel on your next trip. Most likely you were planning to go online and look up the cheapest flights for your next trip and just buy them in cash. Would you realistically go through the hassle of transferring points from your credit card to an airline then redeeming the flights? My guess is that unless you’re an enthusiast, you’re probably thinking that this is just too much trouble.

Therefore, Citi Thank You points and Chase points are probably worth about the same for you. The deciding factor then becomes how you can get the most points.

A welcome bonus is only once, whereas a card could be forever much longer

One of the largest benefits of the CSP is its extremely generous welcome bonus. Citi has had welcome bonuses from time to time, though they are a little harder to find. When Citi does offer bonuses, they are traditionally also in the 50k points ballpark, so extremely comparable to CSP. When redeeming points for rewards, both cards have redemption bonuses of 25% (i.e. 50,000 points worth $625, which is 1.25x $500).

As of today, Citi is not offering a welcome bonus. I get that the $625 can be a compelling reason to get the CSP. But think about this – once you’ve held that card for over a year, what will it continue to do for you? Many of you who are reading this probably already have the CSP – so I challenge you to reconsider after a year.